UCR School of Business Associate Professor of Management Ye Li was asked to provide expert insights on Rational Choice Theory for an article recently published on MoneyGeek.

MG: What is the best way for individuals to apply rational choice theory and use it to their advantage?

Ye Li: Rational Choice Theory is a normative (i.e., what should happen) theory for how people should behave across all kinds of situations. It assumes that individuals decide by comparing the costs and benefits of various options and choosing the one that maximizes their personal advantage. This theory is based on the idea that individuals act rationally, which lots of research suggests isn't always true.

MG: How does rational choice theory impact people’s daily lives when it comes to finances?

Ye Li: Rational Choice Theory impacts financial decisions by suggesting that people should make choices that maximize their financial well-being, not just in the present but throughout their lives. For example, when deciding whether to save or spend money, individuals should weigh the immediate gratification of spending against the long-term benefits of saving. This impacts financial decisions like investing in education, saving for retirement or purchasing cost-effective products and services.

MG: How can people make more rational financial decisions? What are some tips?

Ye Li: This will tend to depend on people's individual financial situations, but here are some general tips:

- Set Clear Financial Goals: Short-term goals such as saving for a vacation, building an emergency fund or paying off credit card debt can help you stay focused and motivated. Long-term goals such as saving for retirement, buying a home or funding your children's education are important as well, but they require more planning and discipline.

- Create and Stick to a Budget: Use budgeting tools or apps to monitor where your money is going. This helps you identify areas where you can cut back. Make sure that your spending aligns with your financial goals. Consider allocating a portion of your income to savings and investments before spending on non-essentials.

- Automate Savings and Investments: Set up automatic transfers to your savings and investment accounts. This ensures that you consistently save and invest without having to think about it. Definitely make sure to take advantage of employer-sponsored retirement plans (401(k)), especially if they offer matching contributions.

- Avoid Impulse Buying: Implement a waiting period for non-essential purchases, especially big-ticket items. This helps you determine if you really need the item or if it’s just an impulse. When doing daily shopping, make a shopping list and stick to it to avoid buying unnecessary items.

- Practice Mindful Spending: Spend money on things that truly matter to you and bring value to your life. This helps you avoid unnecessary expenses and focus on what’s important. After making a purchase, reflect on whether it was worth it and if it aligns with your financial goals.

What Is Rational Choice Theory (RCT)?

In economics, rational choice theory (RCT) is a school of thought stating people’s decisions are based on rational analysis to achieve favorable outcomes. Individuals are calculating costs and benefits to determine which choices can maximize self-interest or are aligned with their beliefs.

Understanding Rational Choice Theory

RCT is a framework used in economics that assumes people are rational. Rationality refers to making efficient decisions to achieve the greatest benefit: If a person faces different choices, they will opt for the one that will provide the most benefit.

Now that we’ve identified rational choice theory, let’s dive deeper into its existence and how it works.

History of RCT: Rational Actors, Self-Interest and the Invisible Hand

The rational choice theory was first introduced in 1776. Well-known economist, Adam Smith, proposed the theory in his book, “An Inquiry into the Nature and Causes of the Wealth of Nations.” Smith also helped developed the theory’s underlying principles. He used the metaphor, “invisible hand.”

The invisible hand explains how unseen forces influence free market economy. Under this, negative connotations of self-interest are refuted.

The theory believes that while rational actors consider their self-interest, they still create benefits for the economy and society as a whole. Thus, RCT has been used to understand behaviors of individuals and the society.

Rational Choice Theory’s Role in Society: Strengths & Discrepancies

There are various theories created to try to explain and understand human behavior. One of these is RCT. It’s used as a predictor of people’s choices. It also assumes quite a bit about the way people choose preferences and goals.

That said, many are disputing its relevance and role in society. Dissenters point out that rationality is not always the basis of decisions. Individuals are often affected by emotions and other external factors like status quo.

Rational Choice Theory’s Strengths and Discrepancies

Strengths of RCT

- It helps make assumptions about a rational actor’s behavior in a certain circumstance and predicts an outcomes.

- It can help explain an individual’s or a group’s behavior.

- It explains rational and irrational decisions.

- RCT is a versatile theory applied in various fields.

Discrepancies of RCT

- The theory assumes that the actor is always rational. That means emotions, innate practical sense and any unconscious behavior are not considered.

- RCT does not take into account the complexity of interactions and human action. It human behavior and assumes logic can explain everything.

- RCT focuses on how individuals ought to behave and make decisions. However, it does not provide cultural context or nuance on possible differences and biases.

How Is Rational Choice Theory Applied in Society?

Among the fields that typically apply rational choice theory is economics. This theory is used to determine buying patterns and can help understand prices, demand and supply.

A good application can be seen in expected utility theory, which states that consumers make purchase decisions based on perceived utility or the satisfaction a product or service provides.

However, economics is only a primary application. Various fields have also adopted this framework to attempt to better understand and predict human behavior.

- Game theory: RCT is considered a fundamental element in game theory, which is used to provide a mathematical framework for the analysis of people’s mutually interdependent interactions. It studies social institutions that have set rules related to the actions of individuals to outcomes.

- Prospect theory: Prospect theory aims to incorporate observed violations to create a more descriptively valid framework when an individual makes decisions under risk. It involves two phases: The editing phase, where an individual edits prospects, and the evaluation phase, where a decision is made.

- Routine activities theory: A subsidiary of RCT, this theory gives a macro perspective on crime. It shows how changing conditions, both social and economic, can influence victimization and the overall crime rate.

- Politics: There are many ways RCT is applied in politics. Politicians may use it to determine the wants of their constituents. Governing bodies and agencies can determine prioritization of projects and policies based on the best interest of society. Additionally, politicians can use it to predict the actions of other leaders.

- Sociology: The application of RCT in sociology focuses on understanding what affects people’s decisions and the impact of these choices on others.

Examples of How RCT Affects Decision-Making in Finances

Among the aspects of life that highly involve decision-making is one’s finances. While behavioral finance believes that a person’s biases, rationales and emotions influence their financial decisions, RCT states that people are rational and unbiased.

The following examples of RCT violations can help you better understand its role in financial decision-making. This knowledge can help you gauge choices when making financial decisions and achieve the best results possible.

RCT Example: Buying Familiar Stocks

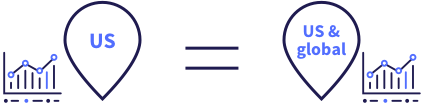

Professional managers often advise diversifying investments by buying from different sectors to hedge the risk. However, many investors tend to buy familiar stocks. A study by Gur Huberman (2001) shows familiarity bias amongst investors, where they buy stocks from local companies. For example, a U.S. citizen is much more likely to invest in a U.S. company, not because it’s a better bet, but because of the company's location.

This shows irrational decision-making. Instead of looking at one’s best interest by diversifying portfolios and buying global stocks, the investor decides based on bias. That means it’s a violation of RCT.

RCT Example: Paying Off Small Loans First

When it comes to loans, individuals tend to pay off smaller loans with low interest rates first before paying off larger loans with high interest rates. In a study, Dan Ariely and his team found that people would rather have fewer accounts than reduce their interest payments.

For example, an individual would rather pay off three small loans of $1,000 each and a 5% interest rate than a $50,000 loan with a 10% interest rate. In the three small loans, the borrower pays $150 interest annually but in the larger loan, they pay $5,000 in interest annually.

Having the desire to take care of small loans first is known as debt account aversion (DAA), which is a form of mental accounting.

This scenario is in violation of RCT. It shows irrationality because paying off larger loans first or starting with those with the highest interest rate and working to the lowest, as in the debt avalanche method, would help the individual save more money. The graph below shows how DAA increases as the interest rate of a debt increases.

RCT Example: Borrowing Money for No Reason

Borrowing money can help businesses. However, taking out a loan is not always a great solution. In some cases, it may not even be a good option.

Despite this, many entrepreneurs and business professionals take out high-interest loans without having liquid cash in the bank. This is an irrational move and a violation of RCT.

For example, taking out a loan at 10% interest while liquid cash sits in your bank earning less than 1% interest hurts your wallet. That is why it’s important to compare a loan’s interest rate to your bank’s saving rate.

RCT Example: Having Inconsistent Preferences

Having inconsistent preferences is not unusual. In fact, 73% of Americans said “they had regrets about their 2021 financial behaviors and decisions.”

Seasonal trends show the correlation between increasing household debt and holiday spending. Americans spent an average of $1,131 during the holiday season in 2021. That led to outstanding debt. In the chart below, you can see higher spending around the fourth quarter.

Credit card use also varies based on credit scores. For instance, people with exceptional credit were seen to put their largest spending on their credit cards. Additionally, only 17% of respondents had not paid off their holiday debts yet.

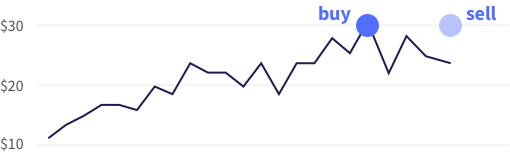

RCT Example: Stock Purchase Price Affects Judgment

Many investors choose to sell profitable stocks to avoid losing stocks because they are afraid of recognizing loss and want to maximize benefits. That said, many also irrationally assume that stocks will increase back to the purchased price even if there is little evidence proving it.

Ritter (2003) provided the example of someone buying a stock at $30, which then drops to $22 before rising to $28. In such a case, most people don’t want to sell until the stock gets above $30. He regarded this investor bias toward winning stocks as the disposition effect.

The disposition effect, which was coined by Hersh Shefrin and Meir Statman, combines anchoring bias and mental accounting. It refers to traders’ tendency to prematurely sell assets that made gains more frequently while keeping assets that have lost their values. This behavior can be considered irrational and it violates RCT.

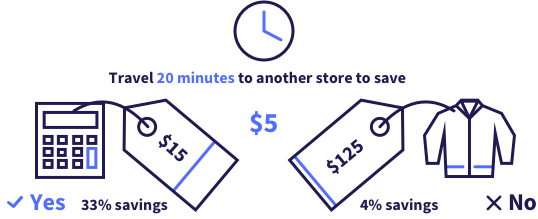

RCT Example: Traveling to Save Money on One Item vs. Another

Money is fungible, which means it’s perfectly interchangeable. For example, people are willing to swap $1 for another $1 without knowing the difference. However, that may change depending on where the money came from.

Thaler (1999) found that consumers were willing to travel 20 minutes to another store to save $5 on a $15 calculator but not to save $5 on a $125 jacket. Following RCT, one should be willing to save $5 regardless of the purchased item. A person acting in their best interest would choose to travel to save $5, regardless of the cost of the original item.

However, in most cases, people view money in comparable terms. In the example given, the $5 savings on the calculator is seen as 33%. However, the $5 savings on the jacket is only 4%.

RCT Example: Fear of Death Doesn’t Correlate With Probabilities

Dissenters of RCT argue that people tend to act according to emotion over probabilities. For instance, dying of heart disease is far more likely than dying in an airplane. According to the Centers for Disease Control and Prevention (CDC), approximately 659,000 people in the country die from heart disease every year. Meanwhile, the National Transportation Safety Board reported 349 fatalities from airplane crashes in 2020. Despite these probabilities, a lot of people fear flying but continue consuming high cholesterol foods.

Additionally, other factors can also affect a person’s fear of death. For example, money or the mere reminder of money can offer soothing effects to help people cope with the psychological terror that comes with the knowledge of mortality. Gasiorowska, et. al (2017) argued that money cues can activate self-esteem which can provide protection against mortality concerns.

RCT Example: Recent News Stories Can Influence People’s Choices

Recent stories in the news can also cause people to inflate the probability of an outcome. For example, Blalock and his team (2009) found that after 9/11, people feared flying and decided to drive more.

While the probability of a car accident is far greater than an airplane crash, many concluded that driving was safer because 9/11 was recent and easily available in people’s minds.

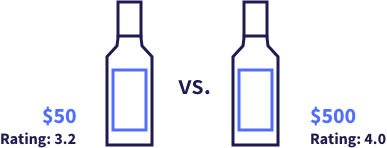

RCT Example: Choosing Wine Based on Price, Not Taste

According to RCT, people should not base decisions on irrelevant factors. For example, if a person wants the wine with the best taste, price should not influence their wine choice. Only the taste should matter. However, that is not how the human brain works. Cambridge University studied more than 6,000 blind tastings and people only preferred more expensive wine when they knew the price (Goldstein et al., 2008).

While the price of wine should have no effect on the taste, people can be irrational. When irrelevant factors influence preferences, there is a violation of the RCT.

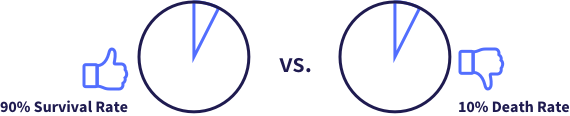

RCT Example: Outcome Rates Change People’s Choices

An experiment conducted by Sox and Tversky showed that 50% of patients were more likely to opt for surgery when doctors described the outcome as having a 90% survival rate as opposed to a 10% death rate.

While the odd of dying are the same in both scenarios, the mere description of the surgery changed the patient’s preferences. Behavioral economists call this phenomena the framing effect and nudges individuals to violate RCT (Lewis, 2016).

Does RCT Help Us Understand People’s Choices Better?

Economic theories exist to find ways to understand how money organizes production distribution and consumption of products and services. For rational choice theorists, the same general principles can help understand human interactions wherein time, approval, information and prestige are exchanged.

The theory states that individuals have to make choices based on their goals and the means to attain said goals. Preferences are based on anticipated outcomes for each action. As rational actors, individuals will choose the course of action leading to the greatest result or satisfaction.

____________________________________

All images courtesy of MoneyGeek